RENU SURESH

Expert

Published on: Mar 26, 2026

New VAT Rules Announced for Precious Metals and Gemstones Traders

In a major advancement for the precious metals and gemstones trading industry, the UAE Ministry of Finance has announced expanded value-added tax (VAT) regulations. Under the newly issued Cabinet Decision No. (127) of 2024, these updated rules introduce the reverse charge mechanism for businesses involved in trading gold, diamonds, and other valuable commodities. This significant change aims to streamline tax processes and support the growth of the UAE’s vibrant trading sector.

What’s Changing?

Previously, under Cabinet Decision No. (25) of 2018, only transactions involving gold and diamonds between registered businesses were subject to the Reverse Charge Mechanism (RCM). Now, with Cabinet Decision No. (127) of 2024, the RCM has been expanded to include more precious metals and stones.

What is the Reverse Charge Mechanism?

The Reverse Charge Mechanism (RCM) is a crucial part of the new VAT regulations introduced by the UAE Ministry of Finance. To make it simple, RCM changes who is responsible for paying the VAT on a transaction between businesses.

- How VAT Normally Works: In a typical business transaction, the supplier provides goods or services to the buyer and adds VAT to the sale price. The supplier then collects this VAT and pays it to the government.

- What Changes with the Reverse Charge Mechanism: Under the new RCM rules, this responsibility shifts from the supplier to the buyer. Here’s how it works:

- No VAT Charged by the Supplier: When the supplier sells goods covered by the RCM to another VAT-registered business, they do not add VAT to the invoice.

- Buyer Pays the VAT Directly: Instead of the supplier handling the VAT, the buyer calculates the VAT on their purchase and reports it directly to the government in their VAT return.

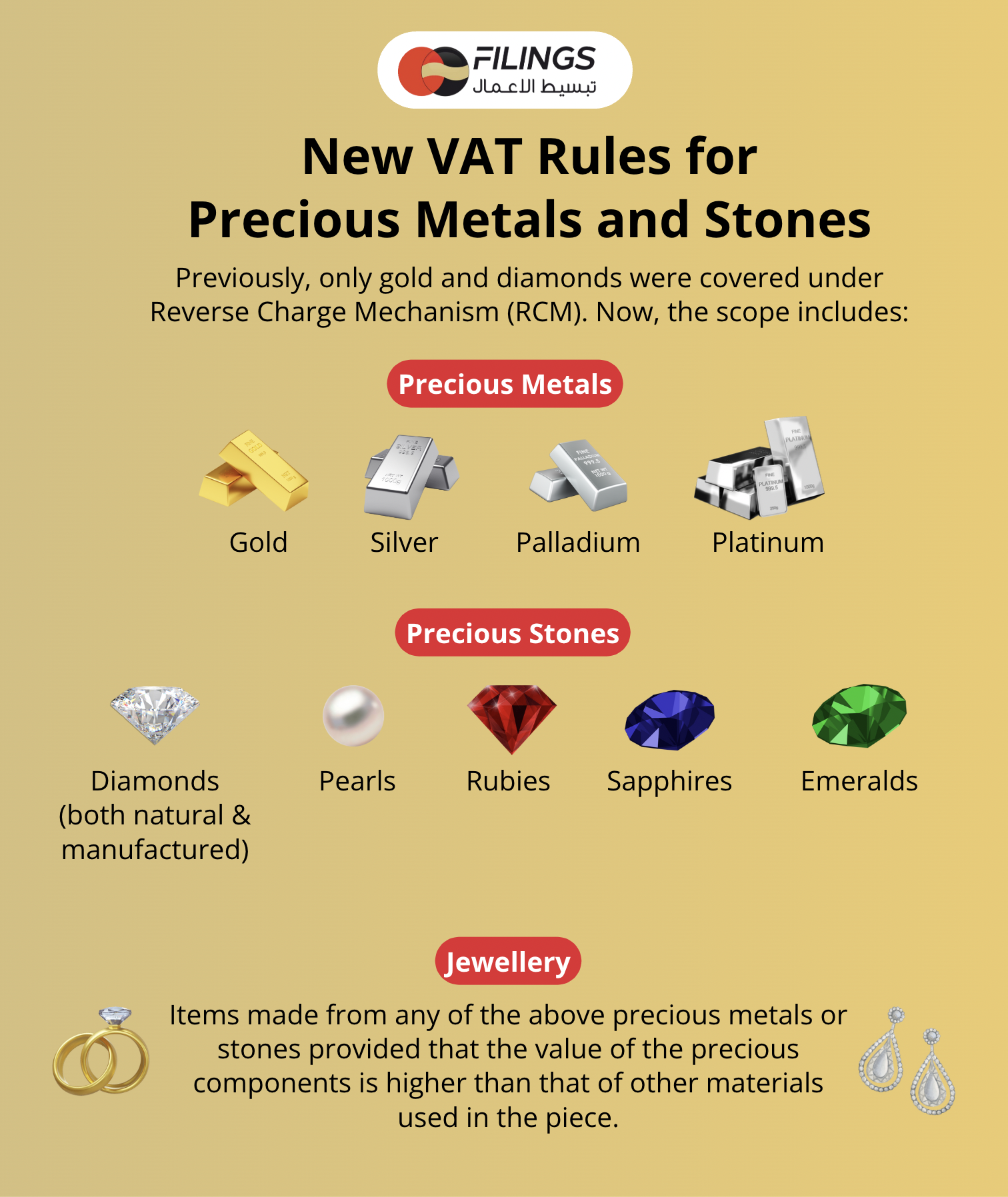

New VAT Rules for Precious Metals and Stones - What’s Included Under RCM ?

As mentioned, The new VAT rules broaden the range of items subject to the Reverse Charge Mechanism (RCM). Previously, only gold and diamonds were covered under this mechanism. Now, the scope includes:

Precious Metals:

- Gold

- Silver

- Palladium

- Platinum

Precious Stones:

- Diamonds (both natural and manufactured)

- Pearls

- Rubies

- Sapphires

- Emeralds

Jewellery:

- Items made from any of the above precious metals or stones, provided that the value of the precious components is higher than that of other materials used in the piece.

How do the New VAT Provisions Work?

Under the new VAT regulations, VAT-registered suppliers are no longer required to charge and collect VAT on the sale of goods covered by Cabinet Decision No. (127) of 2024 to other VAT-registered customers, provided that all stipulated conditions are met. Instead of the supplier handling the VAT, the responsibility shifts to the buyer. This means that the VAT-registered customer must calculate and declare the VAT on their purchases of these goods and include it in their VAT return.

Supplier Responsibilities:

- No VAT Collection: Suppliers do not add VAT to their invoices for eligible goods sold to other VAT-registered businesses.

- Verification: Suppliers must ensure that their customers are VAT-registered and maintain the necessary documentation to support the transaction under the Reverse Charge Mechanism.

Buyer Responsibilities:

- VAT Calculation: Buyers calculate the applicable VAT on their purchases of the specified precious metals and stones.

- VAT Declaration: Buyers report both the input VAT (on purchases) and the output VAT (on sales) in their quarterly VAT returns.

- Direct Payment: Buyers remit the calculated VAT directly to the Federal Tax Authority (FTA) as part of their VAT reporting obligations.

Example Scenario:

- Before the Change: A gold dealer sells gold to a jewellery manufacturer. The gold dealer adds 5% VAT to the sale price, collects this VAT from the manufacturer, and later pays it to the government.

- After the Change: The gold dealer sells gold to the jewellery manufacturer without adding VAT. The jewellery manufacturer calculates the 5% VAT on their purchase and reports it directly to the government in their VAT return.

Below is a summary of the key aspects of the new VAT rules on RCM:

| Aspect | Details |

| Applicable Goods | Precious Metals: Gold, silver, platinum, palladium. Gemstones: Natural and manufactured diamonds, pearls, rubies, sapphires, emeralds.Jewellery: Items where precious components (metals or stones) dominate in value. |

| VAT Rate | Standard Rate: 5%Reverse Charge Mechanism: Applies to specific B2B transactions involving registered traders. |

| Effective Date | January 1, 2025 |

| Cabinet Decision | Cabinet Decision No. (127) of 2024 |

Benefits of Updated VAT Rules for the Precious Metals and Gemstones Trading Sector

The new VAT rules in the UAE bring several important benefits to those trading in precious metals and gemstones.

- By shifting the responsibility of handling VAT from sellers to buyers, businesses can better manage their finances and reduce paperwork, making operations smoother and more efficient.

- These changes also align the UAE with global tax standards, attracting more international investors and strengthening its reputation as a top trading hub.

- Additionally, the new rules help prevent tax fraud and encourage more businesses to register for VAT, supporting the growth and diversification of the UAE’s economy.

Overall, these updates create a more transparent, efficient, and competitive environment for the precious metals and gemstones trading sector.

Key Differences in VAT Rules for Precious Metals and Gemstones

To understand the significant changes introduced by Cabinet Decision No. (127) of 2024, it’s essential to compare it with the previous regulation, Cabinet Decision No. (25) of 2018. Below is a detailed comparison highlighting the key differences:

Aspect | Cabinet Decision No. 25 of 2018 | Cabinet Decision No. 127 of 2024 |

Scope | Only applicable to gold and diamonds. | Now includes gold, silver, palladium, platinum, natural and manufactured diamonds, pearls, rubies, sapphires, emeralds, and jewellery made from these materials. |

Declarations Required | One written declaration stating the use and resale of the goods. | Two written declarations: one for the intended use (resale or manufacturing) and one confirming VAT registration with the FTA. |

Supplier’s Responsibility | Joint responsibility with the buyer if the buyer is not registered. | Suppliers must keep declarations and verify the buyer’s VAT registration but are not jointly responsible if the buyer fails to comply. |

Non-Compliance Handling | Both supplier and buyer are responsible if the buyer is not registered or fails to submit declarations. | Focuses on declarations being submitted; suppliers verify registrations but do not share joint liability. |

Exceptions | Excluded if the supplier knows the buyer is not registered or fails to verify registration. | Relies on declaration submissions without joint liability for suppliers. |

Key Conditions to Qualify for the Reverse Charge Mechanism

To benefit from the new Reverse Charge Mechanism (RCM) under the updated VAT rules, businesses must meet two essential conditions

- Be VAT Registered: Both the supplier and the buyer must be registered for VAT in the UAE.

- High-Value Jewellery: For jewellery, the precious metals or stones must constitute the majority of the item's value. This means that only jewellery where the value of gold, silver, palladium, platinum, diamonds, pearls, rubies, sapphires, or emeralds exceeds that of other materials qualifies under RCM.

Why Register for VAT?

Registering for VAT is essential to fully benefit from these new rules. It helps your business operate more smoothly, manage finances better, and stay competitive in the global market. Don’t miss out on these advantages!

Get Started Today!

Ensure your business is VAT registered to streamline your operations and grow your trading activities. Contact filings.ae experts now to register for VAT and take advantage of the new VAT regulations in the UAE.

FAQs on New VAT Rules for Precious Metals and Gemstones Trader

What are the recent VAT changes for gold and diamond traders in the UAE?

In 2024, the UAE introduced new VAT rules (Cabinet Decision No. 127) that expand VAT regulations for gold and diamond traders. Now, more precious metals like silver, palladium, platinum, and gemstones such as pearls, rubies, sapphires, and emeralds are included. These changes help make tax processes easier and support the growth of the trading industry.

How has the UAE expanded the Reverse Charge Mechanism (RCM) for gold and diamond traders?

The UAE has broadened the Reverse Charge Mechanism (RCM) through the new VAT rules. Previously, only gold and diamonds were included. Now, the RCM also covers other precious metals and gemstones. This means that when a registered business buys these items, they are responsible for calculating and paying the VAT instead of the seller. This shift reduces paperwork for sellers and simplifies tax handling.

What are the overall VAT changes for precious metals in the UAE introduced in 2024?

In 2024, the UAE made several VAT changes for precious metals and gemstones:

- More Items Covered: Includes gold, silver, palladium, platinum, diamonds, pearls, rubies, sapphires, emeralds, and high-value jewellery.

- RCM Expansion: Buyers now handle the VAT payment instead of sellers for these items.

- Effective Date: These changes started on January 1, 2025.

- Benefits: Simplifies tax processes, reduces fraud and supports the trading sector’s growth.

Which precious metals and gemstones are now subject to the new VAT Reverse Charge Mechanism in the UAE?

Under Cabinet Decision No. (127) of 2024, the following items are subject to the Reverse Charge Mechanism:

- Precious Metals: Gold, silver, palladium, platinum.

- Gemstones: Natural and manufactured diamonds, pearls, rubies, sapphires, emeralds.

- Jewellery: Items where the value of precious metals or gemstones exceeds that of other materials used in the piece.

When did the new VAT rules for precious metals and gemstones traders come into effect in the UAE?

The updated VAT rules under Cabinet Decision No. (127) of 2024 became effective on January 1, 2025. Businesses involved in trading the specified precious metals and gemstones must comply with these regulations from this date onward.